pre-ipo

Exited

Airbnb, Inc. was founded in 2007 by Brian Chesky, Joe Gebbia, and Nathan Blecharczyk in San Francisco, California. What began as a way to rent air mattresses to conference attendees has grown into the world's largest online alternative accommodation marketplace, connecting travelers with unique stays across more than 220 countries and regions.

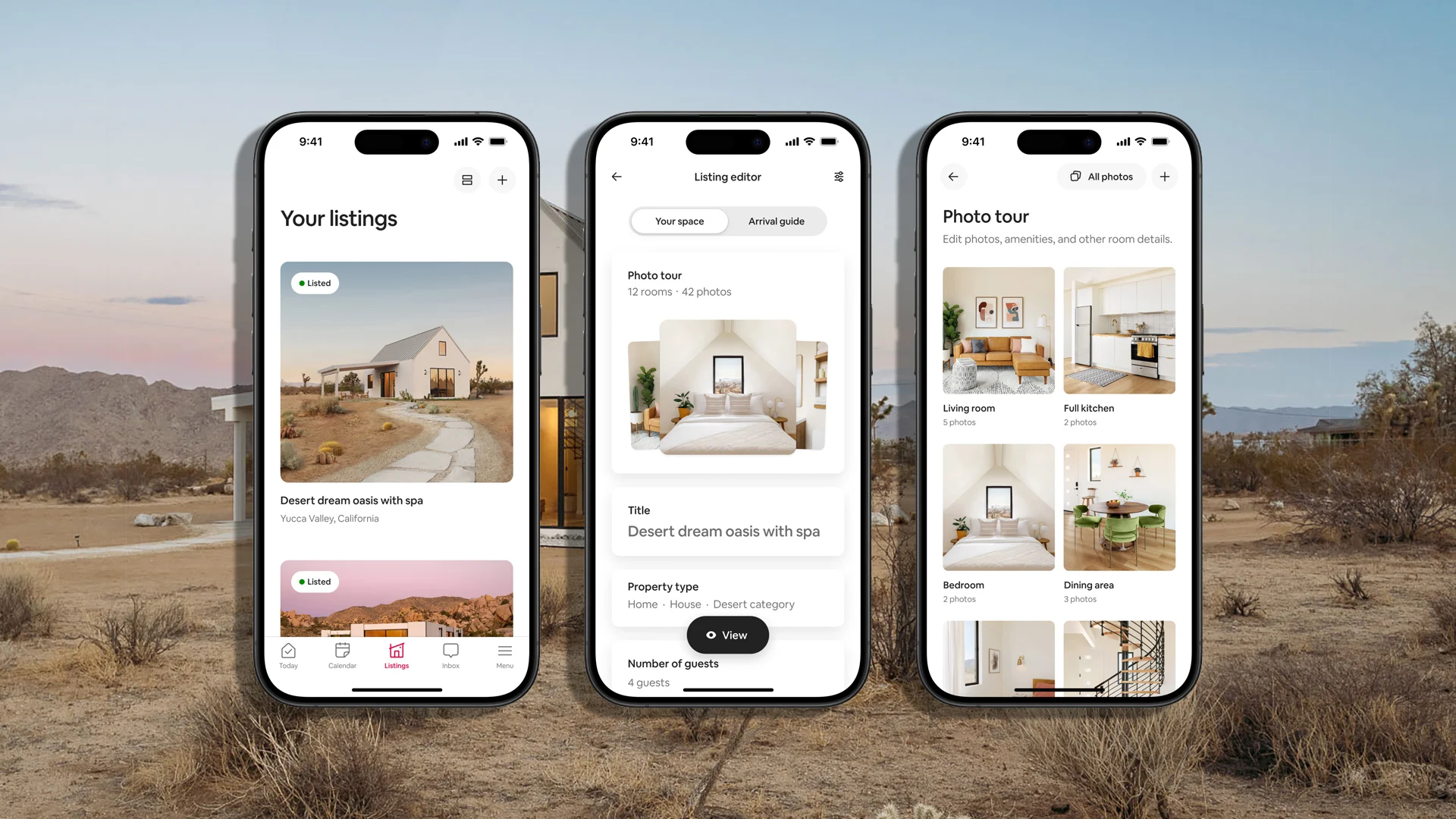

The platform hosts over 9 million active listings — spanning private rooms, entire homes, treehouses, castles, houseboats, and increasingly boutique hotels — managed by more than 5 million hosts worldwide. Over half a billion guests have stayed in an Airbnb, and the company has paid hosts more than $65 billion cumulatively.

Airbnb went public in December 2020 at $68 per share and trades on NASDAQ under ticker ABNB. The company has established itself as a highly profitable marketplace with strong free cash flow, a fortress balance sheet, and an expanding product vision beyond core accommodations.

Airbnb generated $12.2 billion in revenue in 2025, representing 10% year-over-year growth, with $4.6 billion in free cash flow and approximately 35% adjusted EBITDA margins. The company processed 491 million bookings with a gross booking value of $81.8 billion.

Q4 2025 was particularly strong: revenue grew 12% YoY to $2.78 billion, exceeding guidance. GBV surged 16% — the highest growth quarter in more than two years — with 121.9 million nights and seats booked, beating analyst estimates. CEO Brian Chesky stated the company expects growth to "accelerate in 2026," with Q1 guidance of $2.59–$2.63 billion implying 14–16% YoY revenue growth.

Airbnb's geographic revenue mix is well-diversified: 42% North America, 39% EMEA, 10% Latin America, and 9% Asia-Pacific. The company's balance sheet holds approximately $11 billion in cash and investments. Sixty percent of the user base are millennials.

The company is investing in three strategic growth vectors: aggressive expansion into hotel listings to supplement home inventory during peak seasons, scaling the Experiences product, and AI-powered services to improve search, personalization, and host management.

Airbnb is led by co-founder Brian Chesky, who has served as CEO since the company's founding. Chesky restructured Airbnb's organization to function more like a product studio — personally reviewing major product releases and driving the company's design-led culture.

Co-founder Nathan Blecharczyk serves as Chief Strategy Officer. Co-founder Joe Gebbia transitioned to an advisory role. The company employs approximately 8,200 people worldwide.

Publicly traded on NASDAQ under ticker ABNB. Key pre-IPO investors included Sequoia Capital (early-stage investor since 2009), Andreessen Horowitz, Greylock Partners, Y Combinator (W09 batch), General Atlantic, TCV, and DST Global. The company raised over $6 billion in private funding before its December 2020 IPO. Market cap approximately $79 billion as of April 2026.

Airbnb's 9 million+ active listings represent a massive, diversified global supply base. Listings grew 5.1% YoY in 2024. The platform's 5 million+ host base creates a capital-light supply model — Airbnb does not own, lease, or operate any properties, making it a pure marketplace with inherently high margins.

Airbnb ranks third in market share across all travel app providers, behind Expedia and Booking Holdings. However, Airbnb dominates the alternative accommodation segment while traditional OTAs compete in standardized hotel inventory. The expansion into hotels represents Airbnb's move to compete more directly on OTA turf.

Revenue trajectory: $3.38 billion (2020) → $5.99 billion (2021) → $8.40 billion (2022) → $9.92 billion (2023) → $11.10 billion (2024, +12.1% YoY) → $12.24 billion (2025, +10.3% YoY). The company has been consistently GAAP profitable since 2022.

Valuation at approximately $79 billion represents roughly 6.5x trailing revenue and 17x free cash flow — reflecting both Airbnb's mature profitability and questions about whether growth can re-accelerate through new initiatives.

Q: Is Airbnb's growth slowing?

A: Core revenue growth decelerated from 18% in 2023 to 10% in 2025 on a full-year basis. However, Q4 2025 showed acceleration (12% revenue growth, 16% GBV growth), and Q1 2026 guidance implies 14–16% growth. CEO Chesky has signaled that new business lines — hotels, experiences, and AI — are designed to re-accelerate growth. Analysts expect approximately 10% revenue growth in 2026 with further acceleration possible as these investments mature.

Q: How does Airbnb compete with Booking Holdings and Expedia?

A: Airbnb dominates alternative accommodations (entire homes, unique stays, long-term rentals) while Booking and Expedia primarily compete in standardized hotel inventory. Airbnb's expansion into hotels represents a direct push into OTA territory, but the company's brand strength among millennials and its community-driven model differentiate it from the more transactional OTA experience. Booking Holdings remains significantly larger by revenue and has maintained higher growth rates despite its scale.

Q: What are the key risks?

A: Key risks include regulatory headwinds (many cities have imposed or tightened short-term rental restrictions), decelerating core revenue growth, competition from Booking Holdings and Expedia, uncertain ROI on new business expansions (hotels, experiences, AI), potential take rate pressure as the company expands into lower-margin hotel inventory, and macroeconomic sensitivity — travel spending is discretionary and correlates with consumer confidence and economic cycles.

%201%20(1).png)